Portfolio Profile: Conductor Solar

Attacking the Soft Costs in the Messy Middle Market for Solar

This is the first in a series of posts we are going to do profiling some of the investments in our portfolio. Reach out if you have questions, critiques, or want to get connected to the team!

Company: Conductor Solar

Founder & CEO: Marc Palmer

Maybe it’s the civil engineer in me, but one of the areas I’m most interested in is physical infrastructure of small cities. Whether transportation systems, energy systems, climate resilience systems, or others, the specific constraints due to population size, density, and distribution make for interesting challenges. As with anywhere, there is always the question of cost - especially when thinking about public dollars. Small cities can be particularly vexing because they often fit into a “messy middle” - big enough to have complexity, but small enough to be sub-scale for a lot of systems to make financial sense.

We made an investment in Conductor Solar last October because of the way they are breaking down some of these barriers in the solar market. Today I’m going to share a bit about the problem they’re solving, the team and the business, and what could happen if their thesis is right.

Costs of Solar Energy Systems

Solar energy systems are generally broken up into three categories:

Utility: think large ground solar arrays you might see in a field along the freeway - usually 5MW and larger1

C&I/Commercial (“middle market”): think rooftop solar for a small business, school, or non-profit or a community solar project; a bit of a catch-all for everything between Utility and Residential systems - usually 25kW - 5MW2

Residential: exactly what you think it is - solar for the home, usually on a roof - usually less than 25kW3

Obviously these are very different systems in practice, but the basic technology is the same. All three have played a part in the drastic increase in solar energy capacity that has been installed in the U.S. since 2010:

Accompanying this increase in installed capacity has also been a significant drop in the cost of solar, across all three system categories:

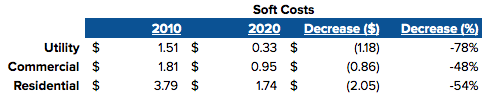

On a dollar per Watt basis, the biggest gain has come from a decrease in hard costs - i.e., the cost of the actual equipment/hardware. Hard cost gains accounted for 71% of the total cost decrease for Utility systems, 78% for Commercial systems, and 58% for Residential systems. Here is how these costs dropped over the 2010s:

On both a percentage and absolute dollar per Watt basis, the gains are fairly consistent across systems:

There is an interesting flywheel happening here - decreases in costs lead to more installed capacity, which leads to further decreases in costs because of the R&D involved to scale, which leads to more installed capacity…and the cycle continues. It’s actually hard to determine exactly which drives which, but the relationship between cost reduction and installed capacity is clear (see Swanson’s Law).

As these systems become more affordable, they become more viable for more use cases. The payback period on installing a system gets shorter, the systems get smaller, and more people and organizations are able to leverage the advantages of renewable solar energy.

The Soft Cost Story

There is, however, one slight complication to this positive feedback loop. While hard costs are a significant part of installing solar capacity, they aren’t the only costs. And in fact, as hard costs decrease, soft costs - think installation labor, permitting, project management, sales & marketing, and anything else not hardware-related - become more and more influential on overall project costs.

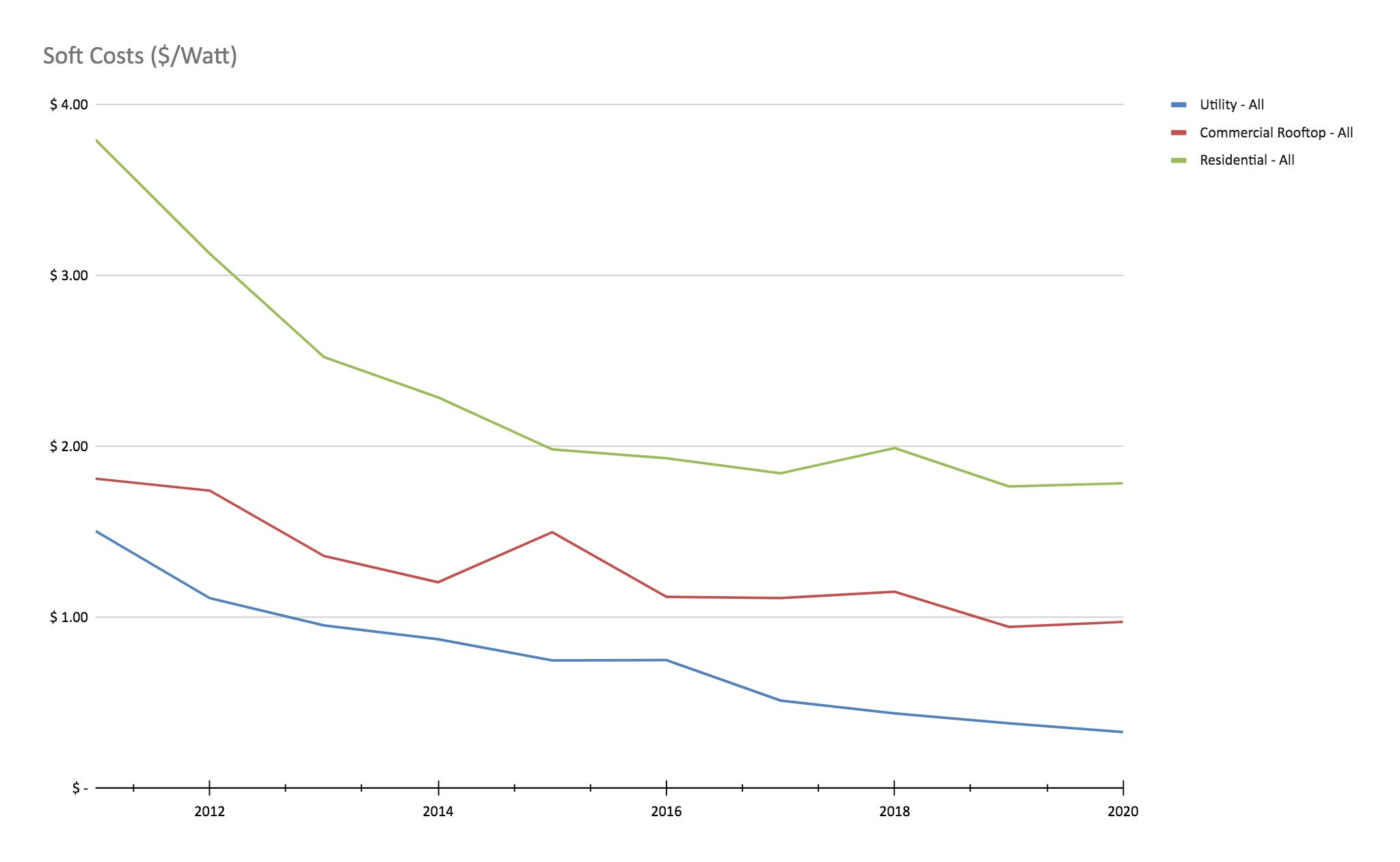

Fortunately, from a dollar per Watt basis, soft costs have also been on the decline since 2010 across all three system types:

But as you may be able to see visually here, the trend is not as drastic - nor as consistent across systems - as the hard cost trend.

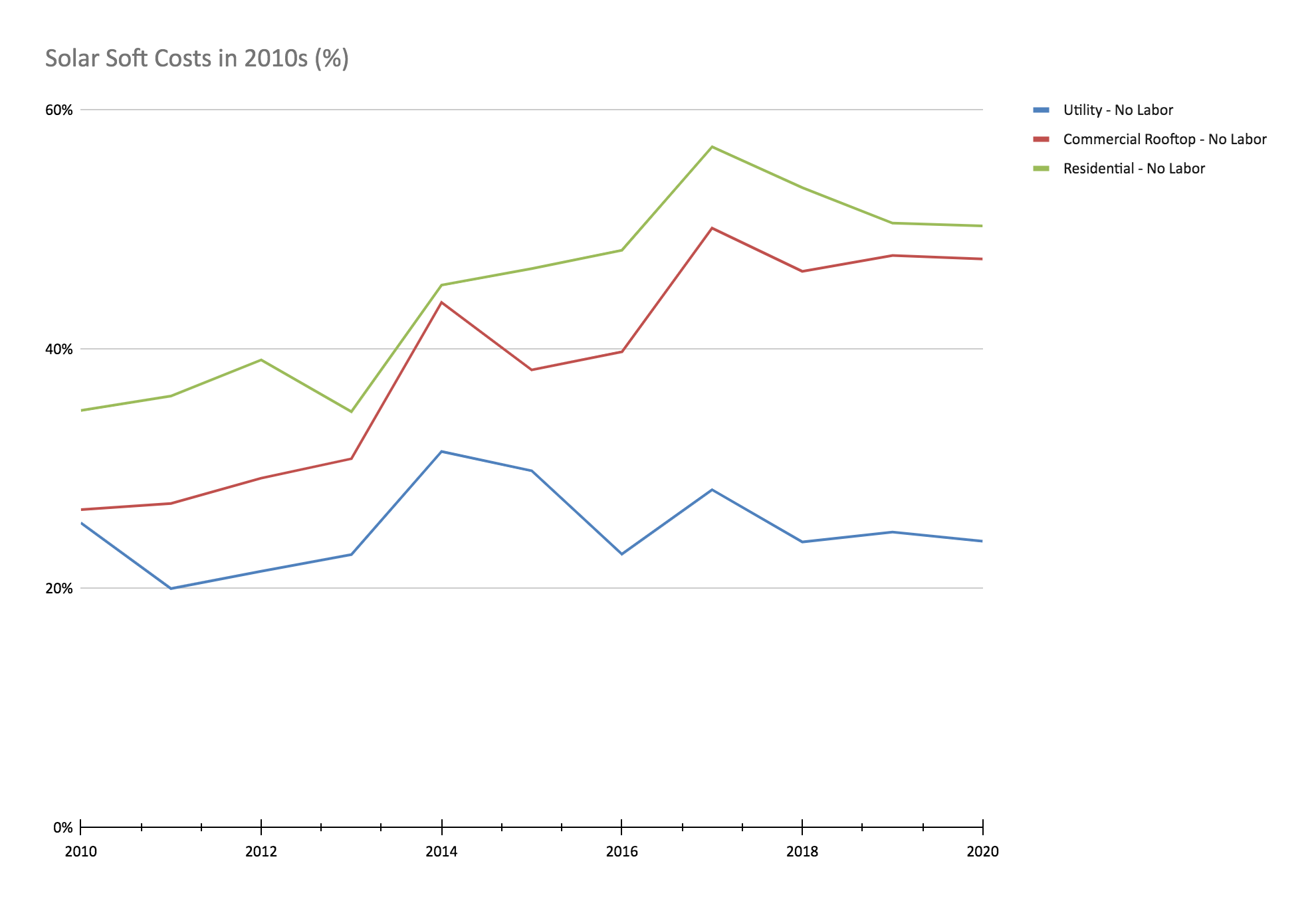

As hard costs continue to plummet, soft costs are making up an increasing proportion of total costs, in all but the Utility-scale case:

And the trend is even more clear if you exclude installation labor from the soft costs:

On an absolute dollar per Watt basis, Utility and Residential systems have seen a comparable decrease in soft costs when you exclude installation labor. But commercial systems have only seen ~50% of that absolute dollar gain.

In most systems, you’d expect the soft costs, as a percentage of overall costs, to decrease as the systems get larger. Commercial system soft costs, despite being orders of magnitude larger in terms of capacity, are on par with Residential systems as a percentage of overall costs.

Therein lies a contradiction:

Compared to Utility and Residential systems, Commercial systems have seen a comparable $/Watt decrease in hard costs, but only 50% the $/Watt decrease in soft costs (excluding install labor).

(more other chart/data takeaways in footnotes4)

“The Messy Middle”

Another way to talk about this is to say that with these Commercial systems, you have Utility-level complexity of soft costs, without Utility-level scale of hard costs.

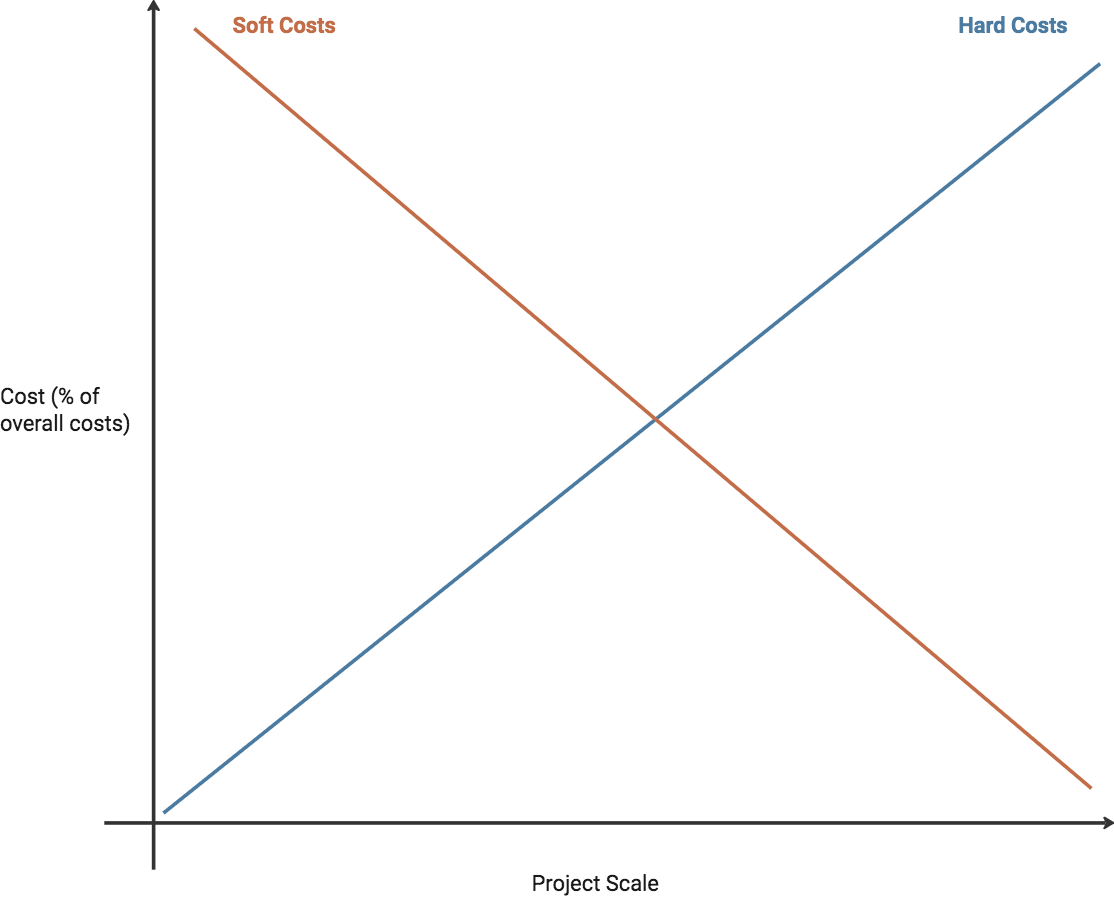

Here is a lazy but helpful way to think about this: If you’re building custom systems, there is usually an inverse relationship between soft costs and hard costs as the size of the system scales. In other words, you need to do a minimum level of work to design a system, no matter the hardware costs of that system. At large scales, these costs get overwhelmed by the hard costs of the system and play a smaller role in the overall budget.

To create systems that make financial sense at small scales then, we turn to standardization. We limit the number of variables and trade flexibility for reductions in soft costs to make these systems possible.

But then a problem emerges. Small scale systems can be standardized only to a certain extent before the complexity is too high. It so happens that the transition happens before you’re at a scale where the hard costs overwhelm the soft costs. And so emerges a “messy middle”:

This step-function in soft costs due to system complexity creates problems when trying to get these projects done. Notice that this is not dependent on the hard costs coming down. That helps with overall costs, but can actually make the step-function even worse.

So what happens? This means that a lot of the middle market projects don’t get done. Either the math doesn’t pencil out from the beginning, or the soft costs kill the project over time. Either way, it means less mid-size solar projects than could otherwise make sense based on the declining costs of the technology.

Costs of Coordination & Capital

This dynamic is not specific to solar energy systems. It probably shows up anywhere you have significant hardware costs and systems that need to be designed and scaled. But what does vary is the components of the soft costs and their respective influences.

In the solar middle market, there are a lot of players that have to come together to make a project happen. At the center of all of these parties is the solar developer. They are interfacing with the end customer, all of the project partners, and anyone involved with the financing. From Conductor Solar:

For solar in particular, there are a lot of different financing types and financing partners. The process of finding them and then making sure they have all the relevant information from all the other parties is time consuming and sometimes just impossible. The longer this process takes the less likely a project is to get done, no matter the long-term ROI case that has been made by the end customer.

As this market grows, there are more incentives, tax breaks, and financing arrangements on who owns the equipment and the rights to the power. This only increases the complexity - making the soft cost problem more prevalent as the market becomes more penetrated.

Why This Matters for Small Cities

Solar is expected to grow in all categories over the next five years:

While the commercial/community solar category might be the smallest by total capacity, we believe it is going to be an important part of the energy equation for small cities. Due to their population and density, the systems in these cities may only be able to be so big. Increasing the ability for municipalities, small businesses, non-profits, and neighborhoods to build solar that fits their needs and capital budgets means that small cities can take part in the transition to renewable energy. The solar capacity of these cities is likely to look more decentralized than other places. To deliver on making this possible, we need to make it easier and more affordable to do middle market projects.

Conductor Solar

Conductor Solar is a managed marketplace for mid-market solar developers to connect to the parties they need to get projects done quickly and cost effectively. They are starting by building a marketplace and workflows for financing arrangements, and will hopefully eventually expand into coordinating other partner relationships needed for these projects.

Their entire goal is simple: lower the soft costs of mid-market projects. This benefits everyone - end users, solar developers, financiers, and partners. Reduced costs and timelines mean more installed solar capacity.

The Team

The team’s advantage can be summed up in one word: experience. Between the team itself and the network of advisors and investors they have built around them, they have every angle of this problem represented: solar financing experience, solar developer experience, solar marketplace experience, enterprise software experience, and more. They have lived the problem, solved the problem in the analog way, and seen what is possible by introducing marketplace technology. This, layered with their existing network of potential customers and marketplace participants, has allowed them to build something that is producing value early and showing the kind of traction that it takes to get something like this out of a cold start. Here is a small sampling of the experience the team brings to Conductor Solar:

Marc Palmer, Co-Founder and CEO

Closed over $1.5B of renewable energy financing projects in his time at Invenergy

Geoff Greenfield, Co-Founder & Board Chair

Co-founder of Third Sun Solar (acquired by Kokosing), a NABCEP board member, and 25 years of experience in the solar industry

Aaron James, COO

Built and managed the national network of solar installers and EPCs for the industry’s leading online marketplace, EnergySage

David Bashien, VP of Product

Head of Digital Operations Analytics for Mass Mutual prior to joining Conductor Solar

The Business

At the residential scale, the answer to the soft cost problem is standardization of products and projects. At the commercial scale, the answer to the soft cost problem is the standardization of process. This includes things like:

Standard project proposals

Standard bid formats

Standard data rooms

Standard financing and legal documents

As these become standardized and therefore predictable, friction in the system is reduced. But standardization is not enough. You need to make it easier for all parties to do things this way, rather than the old way. So you also need workflows. Conductor Solar is taking what is best practice in the industry and making it available for any solar developer that signs up. Those best practices make it simpler for financing partners to evaluate projects and offer bids and for developers to evaluate, negotiate, and finalize deals.

On the business model front, Conductor Solar has thought hard about how to align incentives and encourage network growth. The platform is free to use for both developers and financing partners - Conductor only gets paid if/when a project closes. This success fee forces them to build tooling and standardization that actually gets projects done, while the free use of the platform encourages parties to join, increasing the size and value of the network on the marketplace.

Some might push back though and say, “Doesn’t the success fee model incentivize the team to push toward bigger projects - antithetical to the opportunity?” This is definitely a critique we thought about. At the end of the day, the technology may also make larger projects easier to complete and that could end up driving significant revenue. But even if that is so, it doesn’t detract from the ability of smaller developers and financiers to use the technology and find good fits for their projects. In the same way that AirBnB can at once serve someone wanting to rent a room for a night in South Bend during the depths of January and someone wanting an ocean side villa in the Bahamas, the marketplace drives good matches as long as there is demand and supply, no matter the project size. By starting where the pain is felt the most - the middle market - they are able to profitably attract developers and financiers to the platform and can expand up-market as it makes sense and the tooling and marketplace become more robust.

The Traction

Early results are promising for the platform. They are seeing strong quarter-over-quarter growth in developer and financing partner accounts, total submitted project value, and booked revenue.

And their customers are reflecting the value back to them:

“We had a nearly complete solar project which lost its intended investor. It was kind of a last ditch effort. With Conductor’s help, we closed in 8 weeks with a great new investor under the deadline and ALL parties we happy.”

- Mid-Market Solar Developer

What Happens if This Works

The obvious answer if Conductor Solar is successful is that you will see more commercial, municipal, and community solar capacity installed. This will have an obvious impact on the environment and hopefully also lead to energy savings for these institutions. Additionally, this soft costs problem is not exclusive to solar - there may be opportunities to build adjacencies into other renewable energy technologies or attack other categories of soft costs in the solar market.

But on a deeper level, we are excited about what happens when these energy savings start to come to fruition and these organizations are able to choose how to re-allocate real dollars. We invest in companies because we think, ultimately, they can increase the quality of life for those who call small cities home.

Here’s an example I’ll leave you with.

There is a small community northwest of Indianapolis in Central Indiana called Sheridan. In 2015, the school district decided to invest in solar and rely exclusively on it for their energy needs. As of 2022, that decision is saving the district approximately $1.3M per year.

The best part? They are re-investing those savings into increased salaries for their teachers, making the positions more competitive and allowing them to attract talent to their district.

What else might happen if our schools, small businesses, municipalities, churches, and non-profits had the same opportunity to re-allocate those kind of funds?

We hope to be a small part of the story as Conductor Solar finds out.

If you…

are interested in building for the small city segment…

are already building for the small city segment…

know someone who might be/should be building for the small city segment…

want to contribute expertise to problem profiles…

or want to help us expand our network in small cities…

please subscribe and reach out at dustin@invanti.co.

For datasets I’m using in this post, this means 5 MW to 1 GW systems

For datasets I’m using in this post, this means 100kW - 2 MW systems

For datasets I’m using in this post, this means 4kW - 7kW systems

Other Data & Chart Takeaways:

As hardware has decreased in cost, Utility-scale soft costs have seen a similar cost decrease (hard costs down 83% in $/Watt, soft costs 78% down $/Watt over 2010s)

Non-install labor soft costs as percentage of total costs, are up 79% for Commercial, vs up 44% for Residential and down 6% for Utility over the 2010s

Non-install labor soft costs as a percentage of overall costs of Commercial are almost on par with Residential (48% vs 50%) and double that of Utility (24%)

On absolute dollar basis, Commercial has seen biggest drop in hard costs ($3.09/Watt), but smallest drop in soft costs ($0.86/Watt)

Commercial has seen ~50% of the decrease in non-install labor soft costs of Residential and Utility systems ($0.66/Watt, vs $1.26/Watt for Residential & $1.20/Watt for Utility)

Even though it has the largest absolute decrease in hard costs, Commercial has seen smallest absolute decrease in overall costs ($3.96/Watt vs $4.14/Watt for Residential & $4.92/Watt for Utility)